Question 1

How does this support a trustee's duty to maximise charity assets?

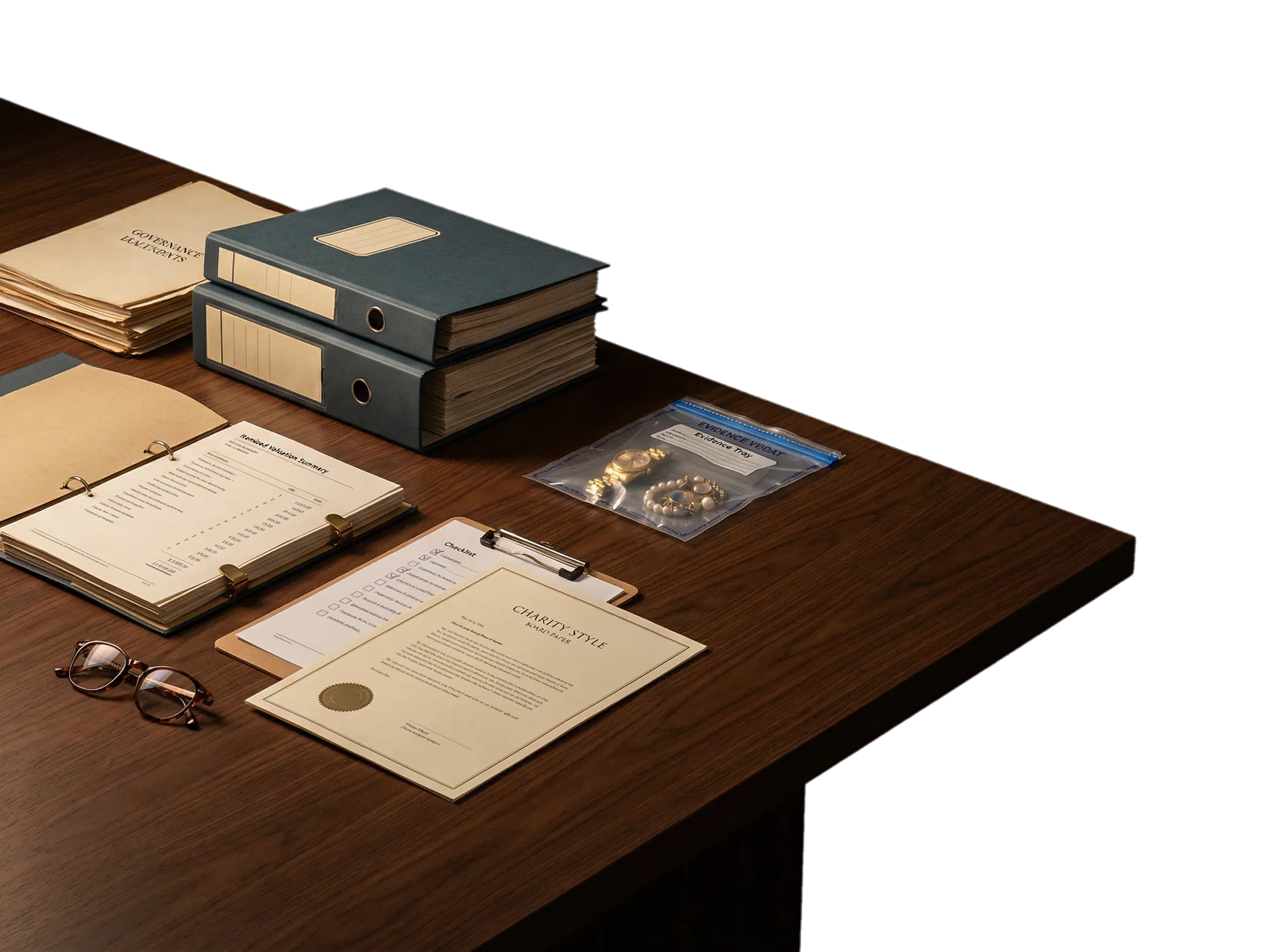

The process is built to replace guesswork with evidence. Precious metals are assessed using XRF testing and priced against the LBMA PM fix. Watches, antiques, and wider collectables are considered against current auction comparables. Each parcel receives an itemised valuation commitment in writing, which helps show that specialist donations were not handled casually or sold on instinct alone.

Question 2

How do you stop personal benefit and make sure the money lands correctly?

Payment is made only to the charity's registered bank account. It does not go to an individual, a shop till, or an informal suspense arrangement. The account is verified against the Charity Commission register during onboarding. That restriction is simple, but it matters. It narrows the fraud surface and gives trustees a cleaner control line to rely on.

Question 3

What audit trail and record keeping does the charity receive?

Every parcel is paired with written records, not just a payment. The charity receives an itemised valuation and a trustee-friendly PDF summary suitable for internal circulation, finance review, or file retention. Tracking, receipt, valuation timing, and banking route all support the underlying record. If you are building an internal pack, that documentary layer is often as important as the price itself.

Question 4

How is reputational risk handled when a charity uses a specialist buyer?

The answer is seriousness, specificity, and clear boundaries. Vintage Piggy is positioned as a UK specialist service for registered charity shops and head offices only. The process is not dressed up as a general public offer. It uses documented postal handling, transparent payment rules, and a clear right to decline and receive items back free of charge. That tone matters when trustees assess reputational exposure.

Question 5

How is data protection handled under UK GDPR?

The charity remains the data controller for its own donor-facing processes. Vintage Piggy handles the information required to operate the valuation and payment route, using UK GDPR-aware handling rather than casual messaging practices alone. In practical terms, the process should be treated as a controlled commercial service relationship, not an informal chat thread without retention or responsibility boundaries.

Question 6

What will a Charity Commission due diligence file actually contain?

The due diligence file should contain the charity-only service description, the registered-bank-only payment rule, the valuation method outline covering XRF and market comparables, sample reporting format, contact details, and the no-exclusivity terms. In other words, the charity should be able to evidence who the operator is, how value is assessed, how funds move, what records are issued, and how the relationship can be stopped.

Question 7

What happens if the charity wants to stop using the service later on?

There is no exclusivity, no minimum volume, and no lock-in requirement. If a charity stops, parcels already in flight still follow the agreed process to conclusion, including valuation and payment where the charity accepts. That continuity point matters. Exit should not create confusion around ownership, records, or money that is already moving through the system.